By Jack Brady

It’s been a pretty eventful 6 weeks since we published our initial outlook on 2019. Trade tensions have continued to ebb and flow, and the U.S. government shutdown ended uneventfully. The Fed has continued its “wait and see” approach to rate hikes, and as of Wednesday afternoon it looks like Powell may end the Fed’s balance sheet normalization at the end of 2019.

Since our 2019 outlook was always meant to be dynamic, we’re going to be revisiting a few of our “base case” assumptions about the global economy and the likely path of Fed policy that we posted back in January.

As a reminder, our three base case assumptions for 2019 were as follows:

1) Massive contraction in global liquidity.

2) We’re late cycle.

3) Powell is no Volcker.

The assumption we’ll be revisiting in this post is the first, in which we assumed a steady balance sheet runoff on the part of the Fed, and no substantial easing on the part of global central banks. We’ll also be revisiting the likely impact of the Fed’s balance sheet runoff.

Our Updated View On Global Monetary Policy:

While we still don’t expect any substantial easing out of the major global central banks (we’re talking ECB and BoJ here — cuts from smaller banks such as the RBI aren’t particularly significant in our view), we are moderating our view on expected global tightening. After yesterday’s Fed minutes indicated that Powell intends to end balance sheet normalization this year, we see little reason to expect substantial tightening out of the Fed any time soon. Just three months ago, Powell claimed that bond maturities were “on autopilot,” so this drastic capitulation on his tightening plans indicates to us that the Fed is likely going to be on hold for a while.

Remaining Balance Sheet Normalization Poses a Mere 1% Headwind to U.S. Equities:

We have also updated our views on the likely impact of the Fed’s balance sheet runoff this year. Initially, we had said that balance sheet normalization would be a major headwind to global markets in 2019, but we no longer believe that is the case.

According to the New York Fed, an additional $312.6 billion of Treasuries will roll off the Fed’s balance sheet by the end of 2019; so will an additional $5.5 billion of Fixed Rate Notes and an $600 million of Agency debt and TIPS. This brings total expected tightening for 2019, and for the foreseeable future, to $318 billion.

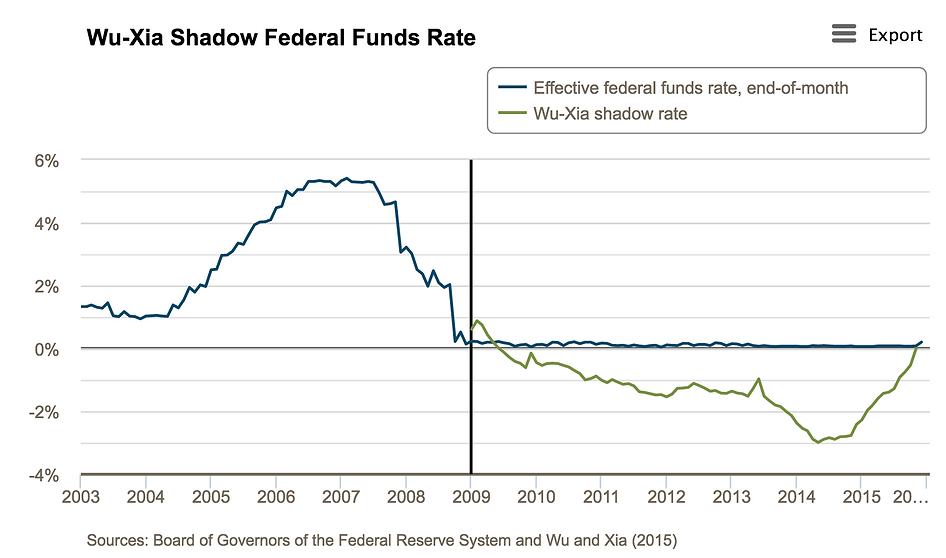

Using the so-called “shadow Federal Funds Rate” model developed by Wu & Xia at the Atlanta Fed, we have attempted to back out a reasonable value to assign to quantitative tightening, in terms of equivalent Federal Funds Rate hikes.

If we assume this model is correct, then the peak of the Fed’s $3.5 trillion Quantitative Easing program that ran from 2009 to late 2014 corresponded with a “shadow rate” of -3% (see below). With the Fed Funds rate pinned at zero that entire time, one can assume that $3.5 trillion of quantitative easing equated to roughly 12 rate cuts, so about $290 billion dollars of quantitative easing is needed to replicate the effect of one rate hike. Ignoring the fact that quantitative easing likely experiences diminishing marginal returns, we estimate that $290 billion of quantitative easing equates to approximately one rate cut, and vice versa.

Note that the so-called “Shadow Rate” bottomed out at -3% in late 2014, coinciding with the peak of the Fed’s QE program. Source: Federal Reserve Bank of Atlanta

Note the Fed’s balance sheet peaked at roughly $4.4 Trillion in late 2014, rising from just under $900 billion pre-crisis on account of their ~$3.5 trillion QE campaign. Source: Board of Governors of the Federal Reserve System

Based on this simple estimate, the threat of the Fed’s balance sheet reduction is much smaller in size than we initially thought. The $318 billion of quantitative tightening that is scheduled for the rest of 2019 should equate to barely more than one rate hike.

Turning back to the path of risk assets, we can use the seminal 2004 paper by Kenneth Kuttner and Ben Bernanke to determine the likely impact of this quantitative tightening on the S&P500. Their paper, which analyzes the reaction function of the stock market to Federal Reserve policy changes, indicates that a 1/4 point cut in the Fed Funds rate generally correlates with a 1% rise in the S&P500. By this logic, the $312 billion in bonds rolling off of the Fed’s balance sheet over the next 10 months represent a headwind of little more than 1% to U.S. equity benchmarks.

The bottom line is that our fears regarding a “massive liquidity contraction” were likely overblown. However, our contention that the Fed is done with rate hikes for now and that the economy is very late-cycle remains in tact, as we have seen little evidence to the contrary over the past month and a half. Our moderated expectations regarding balance sheet normalization merely mean that this rally may have a bit more room to run than we originally thought.

How Does This Change Our View?

At the end of the day, recent developments have only strengthened our conviction that it’s time to sell this rally, or at least to dial back equity exposure significantly. The Fed’s capitulation on rate hikes and balance sheet normalization, along with broadly soft global economic data, indicates to us that the Fed is done hiking for this cycle because they think they have finally broken something. We expect the mechanical rally in stocks to continue as interest rate expectations are revised downward, followed within a few months by a recession and substantial drawdown in global equities.

We’ll conclude with a chart that we pulled from our Macro piece published in December (please ignore the commentary on this graph for the purposes of this discussion). What this chart shows is that there is typically a knee-jerk rally in the stock market after the Fed ends a tightening regime, but that the weak economic fundamentals that cause the Fed to do so eventually win out after a few months. In our minds, this market remains a rally that you want to sell, in spite of weaker-than-anticipated headwinds from quantitative tightening.