By Kyle Sung

Company Overview

Starwood Property Trust (STWD) is a real estate investment trust focused around real estate and infrastructure. STWD is one of the largest loan originators of any institution, and currently provides commercial, residential and infrastructure loans. The company’s current portfolio of around 16 billion dollars contains 4 business segments: real estate lending, real estate investing and servicing, property, and infrastructure lending.

Investment Thesis

I recommend shorting the stock because the company is overvalued compared to its peer group, it faces interest rate risk, recessionary risk (due to potential yield curve inversions and weak housing market), and dividend unsustainability.

The company’s extensive investment in variable rate assets exposes it to significant interest rate risk. To put this risk into perspective, around $8 billion of STWD’s $10.3 billion loan portfolio is comprised of variable rate loans. The ratio decreases when considering the $8 billion of loans are all being held for investment, resulting in a ratio of 8/9th of loans are HTM (the $8 billion includes 6.7 billion in commercial loans, and 1.3 billion in infrastructure loans). Approximately 84.9% of RMBS and a tenth of CMBS’ that STWD reported under the fair value option are variable-rate.

Given the adjustable-rate nature of commercial mortgages and housing loans, interest rates and the net asset values of STWD’s portfolio are directly related. Thus, as interest rates fall, the net asset value of STWD’s portfolio stands to fall. Given current economic standings, including the Sino-American trade war, low manufacturing numbers, housing, slowing job growth and business investment, it is extremely more likely that the Federal Reserve will cut rates rather than raise them in the near future.

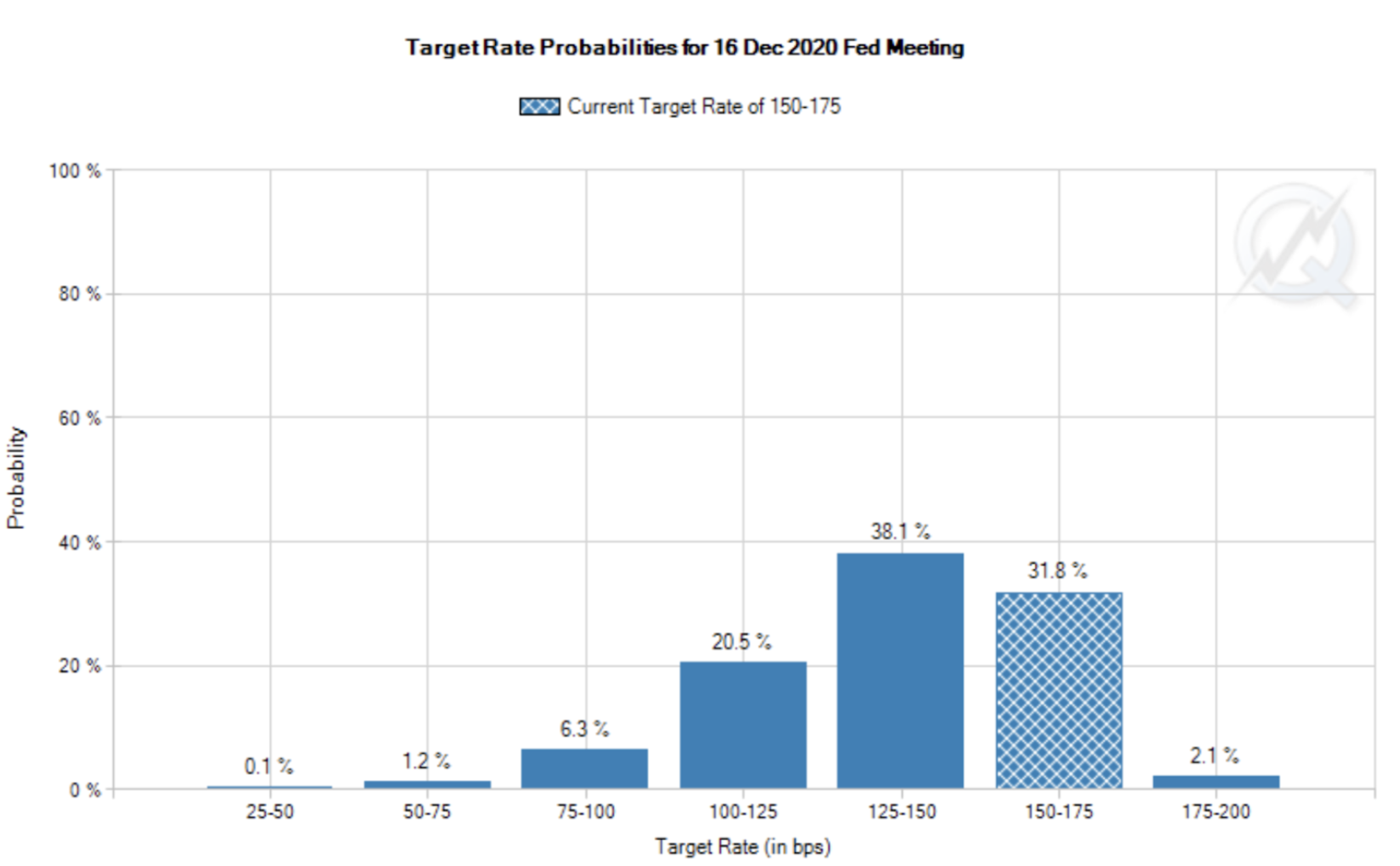

We can check the probabilities of future Federal Reserve rate cuts by looking at the Federal Funds Futures markets. According to a figure by CME Group (pictured above), the markets are currently pricing in a 66.2% chance of at least a 25bp rate cut, with only a 2.1% chance of a hike by the 2020 December FOMC meeting.

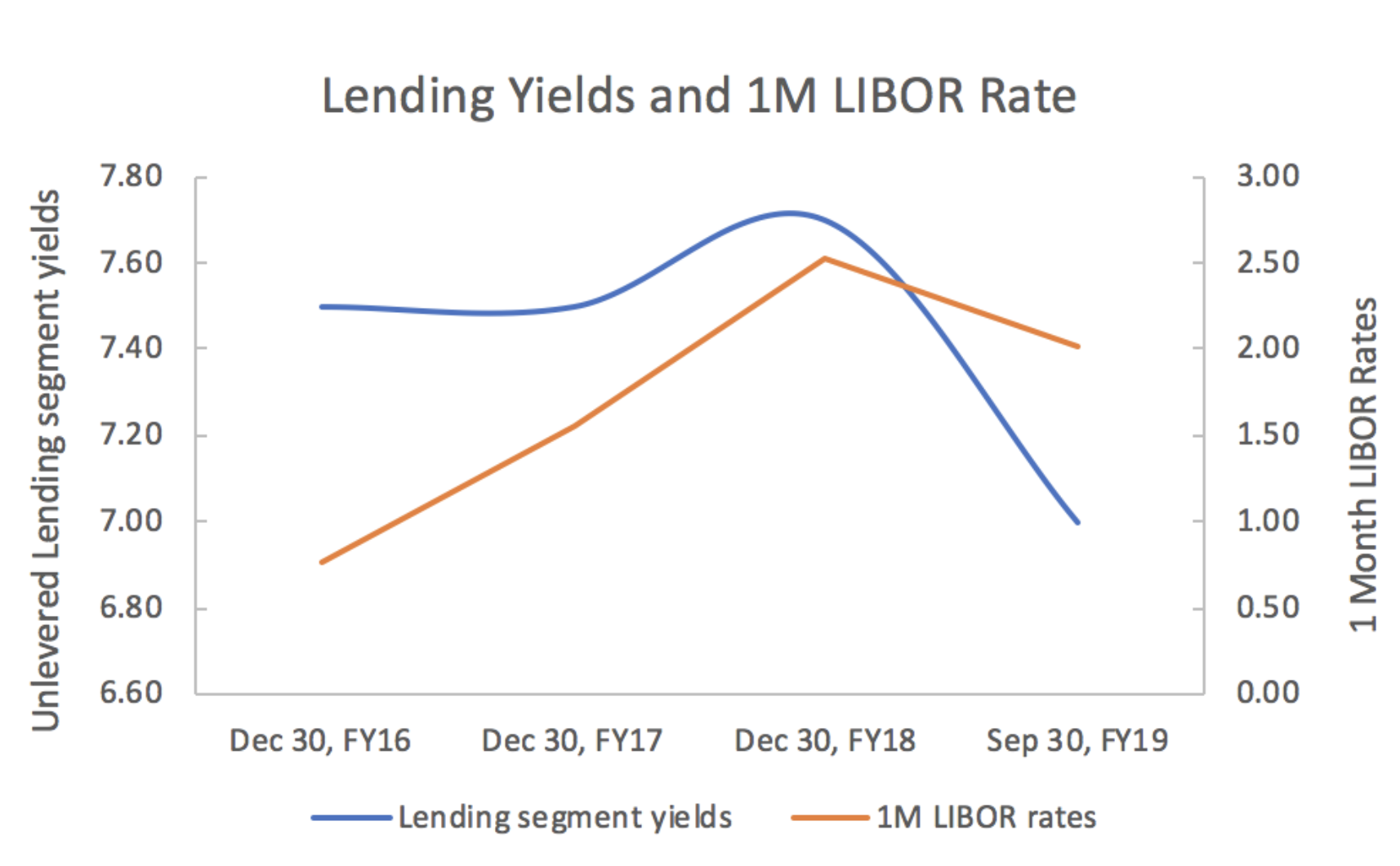

LIBOR rates have steadily climbed between 2015 and 2018. In FY18, STWD saw an increase of yields from FY17’s 7.5% to FY18’s 7.7% from its Commercial and Residential loans segment. The increase, while not overly substantial, was offset by compression of interest rate spreads in credit markets and a decrease in yields from fixed-rate residential loans. As seen in the figure below, there exists an observable, direct relationship between STWD’s loan yields and interest rates, and as the current global economic outlook worsens, we expect to see a decrease of yields across STWD’s Loans and REIS segments as a result of cuts to LIBOR and other applicable rates.

STWD management estimates interest income will drop to -$53,416,000 in response to a 100bp drop in LIBOR, which will likely be offset by decreasing debt interest expenses, which management paints off as very likely to have an accretive effect on diluted EPS. This implies that STWD’s debt expenses are more sensitive to interest rate changes than its interest income, but how is that possible given a REITs’ nature of borrowing at low rates to capture interest rate spread? Whatever the case, future interest rate cuts will act dominantly as a revenue headwind – and potentially a catalyst for my investment thesis.

Like all mREITs, STWD’s profits depend on the interest rate spread between the short term rates the company uses for financing and the higher yields of mortgage loans and mortgage-backed securities. The classical problem with this business model is the mREIT’s exposure to yield curve inversion – when short-term rates drop lower than long-term rates, effectively turning revenue of STWD’s loans and REIS segments negative. While the company’s 2.7x debt/equity ratio is low for a REIT, we nevertheless cannot forget that the ratio acts like a multiplier. For example, as of September 30, 2019, STWD’s available-for-sale RMBS holdings come with a weighted average spread between repo/30 yr mortgage rates of 1.24%, which, when multiplied by 2.7x debt-to-equity, results in an effective spread of 3.35%. Because STWD’s portfolio is incredibly complex, it’s difficult to estimate the exact risks associated with inverted yields on every interest rate spread for every type of asset STWD owns. But this risk exists, and should be a major cause of concern given the current uncertainty present in the domestic and global macroeconomic context. S&P Global Ratings estimated recessionary risk at 30%-35% in the next 12 months at the end of September this year. If history tells us anything, there’s also a 30%-35% for a yield curve inversion in the next 12 months.

In addition to STWD’s exposure to changing interest rates, the company faces a stagnating mortgage and housing market. After a weak start to the year, the housing market gained some momentum in the summer but it is unclear if that will prove sustainable. The pace of existing home sales accelerated in July and August only to fall back in September, according to the National Association of Realtors. The average 30-year fixed mortgage rate rose 7 basis points to 3.96% from 3.89% a week ago. Unwavering mortgage rates, in addition to a shortage of housing, are causing concern among economists, even though the 30-year rate has decreased some 100bp y/y. The current state of the housing market will play directly into STWD’s ability to originate new loans and populate properties.

Given that 83% of the current loan portfolio is first-time loans, STWD’s loans segment is very dependent on the state of the consumer as a part of the economy and the housing market. Economic slowdowns tend to drag the first-time mortgage market into the mud, which would mean lower commercial lending revenue. As for the Property segment, in the 9 months between December 31, 2018 and September 30, 2019, the occupancy rate has fallen among most of the property portfolios that STWD own, with the most startling drop occurring in STWD’s Multifamily-residential Ireland portfolio – a drop from 100% to 81% in 9 months. This drop correlates to this year’s rising housing costs driven by shortages of affordable housing along with a global economic slowdown.

In my research, I have encountered resources deterring consumers from taking long-term mortgages at times of recession, since rising rates after the recession can increase your risk for default. It is possible that home and business owners are deterred from taking mortgages given the current uncertainty among interest rates and the economy. Basically, a recession would produce deep, structural adverse effects among the real estate markets that could potentially disrupt STWD’s ability to generate revenue.

Lastly, I would like to discuss STWD’s dividend unsustainability as a result of poor/mediocre fundamentals.

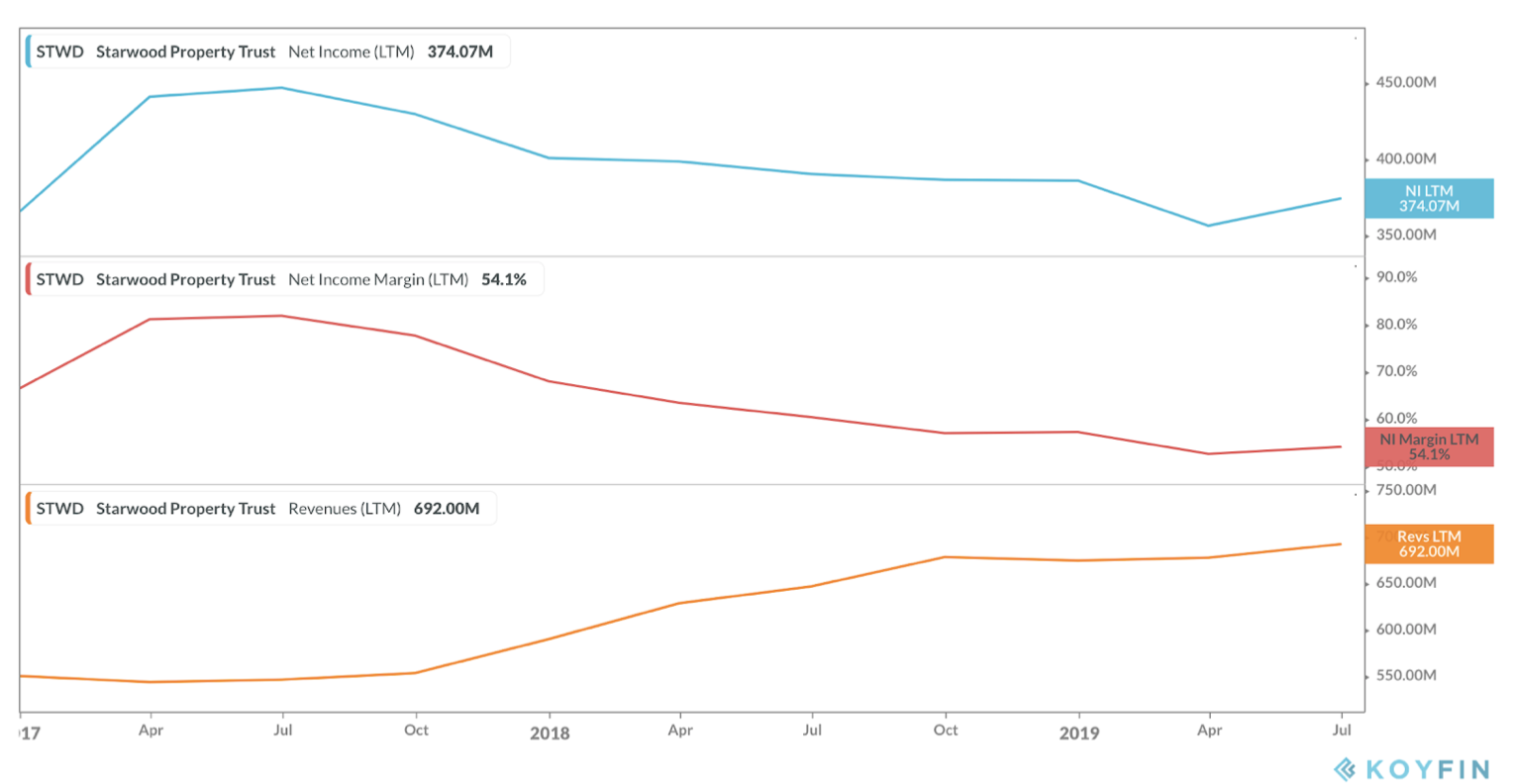

In the graph above, we can observe that while revenue has been increasing over time, the company’s net income margins and net income have been trailing. This company is a case where increasing revenues doesn’t tell the whole story; STWD’s EPS has fallen roughly 7% per year over the last five years, but the company has lifted its dividend 17% per year on average. Its high payout ratio of 142% last fiscal year (FY18 net income/share = $1.42, dividends per share = $1.92) raises concerns that the company’s dividend yield is unsustainable and increases the likelihood for dividend cuts in the future. The company’s bleeding actually matches STWD’s decreasing cash and cash equivalents, suggesting that the high dividends may have been partially funded by its cash reserves.

Dividend cuts, especially from a REIT, will make the stock less attractive to investors, prompting less buying and more selling of STWD shares, which would drive the price per share lower, supporting the investment thesis.

Valuation

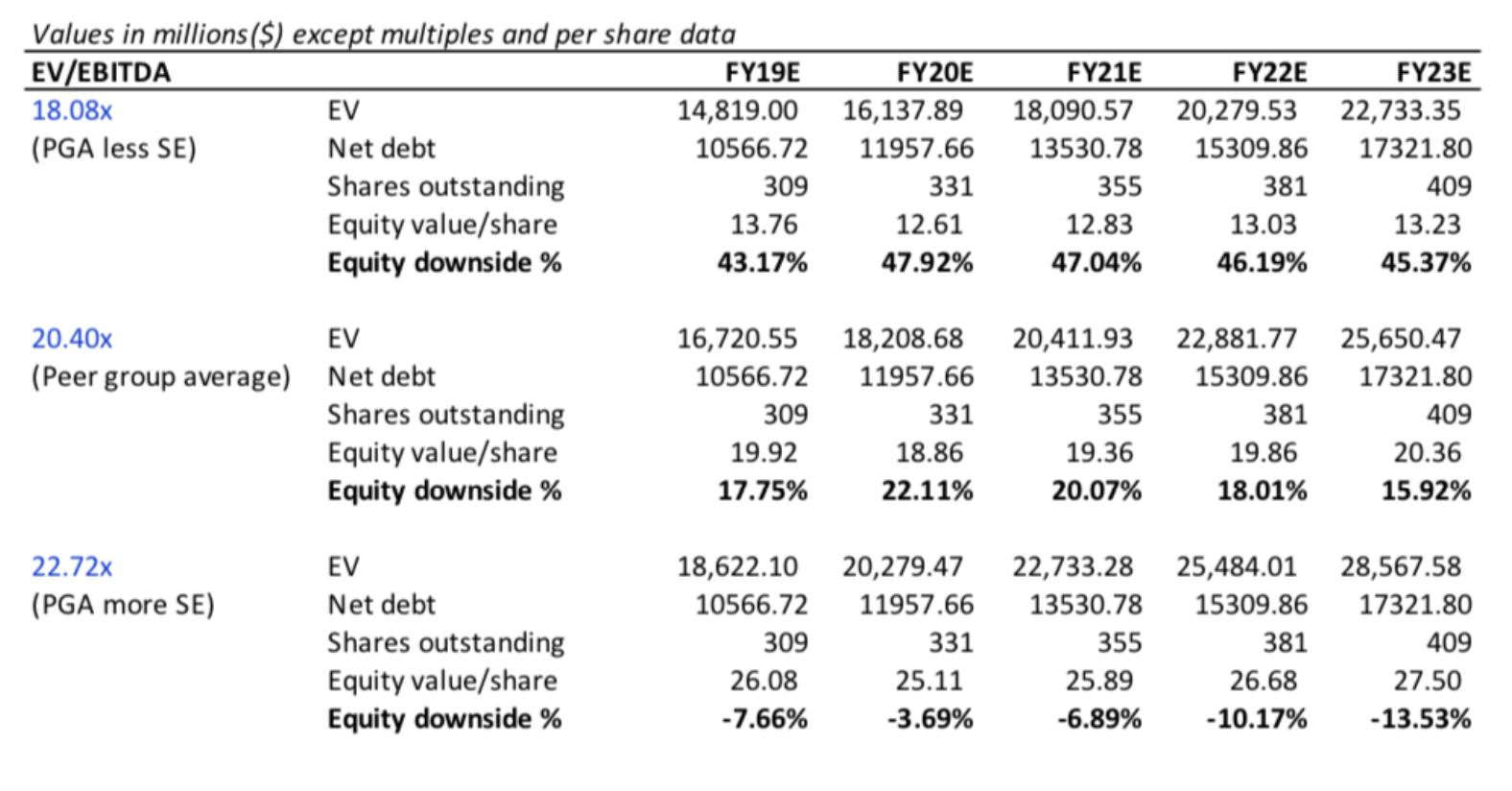

I used peer universe median EV/EBITDA multiple to complete valuation by projecting STWD EBITDA to FY23 and calculating equity value per share based on forecasts. Some key assumptions include: peer group average EV and EBITDA increase proportionally through FY23E, consensus estimates for EBIT for FY19-20, and average EBIT growth rates from then until FY23, and conservative increases in debt at 13% CAGR. Positive equity downside indicates percentage decrease from the current price per share of $24.22. Assuming the company’s multiple compresses to the peer group average, there is a potential profit opportunity of roughly 16% through FY23.

Risks

Better than expected earnings Q4 could threaten the investment thesis. Overperformance could trigger investor confidence in the stock and decrease the likelihood of dividend cuts, increasing price-per-share.

Better than expected economic status could increase confidence in the housing and mortgage markets and overall markets.

Markets price in a 2.1% chance of a rate hike within 12 months of December 2019.

Investors should be cautious when shorting around the ex-dividend date, which could see increased volatility in share prices.

Catalysts

While it is unlikely that the Federal Reserve will cut interest rates for the third time this year in the FOMC December meeting, it remains highly possible that the market may be seeing rate cuts early next year.

Economic data is a major focus of the stock market, and given poor conditions in geographical loans such as the Eurozone, as well as uncertainty in the United States, STWD’s global portfolio may become collateral damage in a global economic downturn. If/when the dividend yield is lowered by management, the price-per-share will likely decline.