By Nilay neelaveni and Osamah Qatanani

Introduction:

Many investors are likely to remember 2018 for its ups and downs. In the US markets right now, it is hard to find safe places to invest where even the safest DOW equities have taken a precipitous plunge (Since the selloff in October and as of today, Goldman Sachs (GS) lost 18.2%, Exxon Mobile (XOM) fell 11.5%, and FedEx (FDX) tumbled nearly 25%. The Federal Reserve’s decision of raising interest rates coupled with the growth in the CBOE Volatility Index (VIX) further worry investors who are already concerned over where we are in the business cycle. Given a bearish outlook on the market, an attractive investment may become harder and harder to find. Catalyst Biosciences (CBIO), however, is an interesting investment opportunity due to its promising science and unique financial situation.

Our Opinion:

CBIO’s investment potential stems from two important factors. Like any pharmaceutical company, CBIO is valued by the overall success of the drugs that it creates. It’s main product, MarzAA, and its second, DalzAA, are the two main drugs that make up its valuation. We’ll delve into the specifics of both of these drugs and their potential below. The second factor, the more interesting one, is its finances (In fact, we debated for a while whether the science or the finance was more interesting, so we went with the more senior opinion). CBIO currently has ~$130 Million in cash on its balance sheet. However, it’s only trading at a $113 Million valuation; that’s 13% below its value in cash holdings. Hence, not only is there the opportunity to invest while its at a low valuation, you are also being paid to own exposure to its drug pipeline.

How MarzAA Works:

If the intriguing financial situation is not convincing enough, the science behind Marzeptacog Alfa (MarzAA), CBIO’s flagship drug, certainly speaks for itself. MarzAA is unique in the way it subcutaneously (SQ), meaning self administered shots into the belly, treats hemophilia A and B, a disease that does not allow red blood cells to clot properly. The alternative method of Intravenous Therapy (IV) is often very inconvenient for hemophilia patients. For example, Sami, a friend and hemophilia patient, said: “When I was younger, it was very difficult to meet up with friends because of the long and tedious IV process done in a Children’s Hospital 20 miles away from me. It would take out so much time from my day and it also left me with needle scars that would embarrass me in school.” Sami and so many other hemophilia patients would greatly prefer this style of treatment than the standard IV process.

Digging Through MarzAA’s Scientific Results Jargon:

After people with hemophilia use MarzAA in regulated amounts, their annual bleed rate (ABR) went from as high as 28 (where 22% of their day consisted of bleeding) to as low as 0 (a 90% reduction in ABR).

Source: catalystbiosciences.com. The red bars are pre-treatment ABR and the green bars are during treatment.

Following the successful set of trials, the Food and Drug Administration (FDA) gave MarzAA an Orphan Drug Designation (2017). An Orphan Drug Designation is given to drugs that have proven to be safe and effective in preventing rare diseases, and have also been evaluated by the Senate.

How DalcAA Works:

CBIO is not a one-trick-pony. It has not one but two star products in its pipeline! Because hemophilia severity is greater when there is a deficiency in Factor IX (FIX), CBIO is also working on the production Dalcinonacog Alfa (DalcAA) to regain FIX activity.

DalcAA Has Its Own Scientific Results Jargon:

While DalcAA also shows great results of maintaining FIX activity at about 12% (which is about average), there was a snag in the plans the summer of 2018 when two subjects developed neutralizing antibodies (nAb) to the drug. This means the subjects’ immune systems were unable to accept DalcAA, simultaneously leaving them untreated. Further research indicated they are cousins and thus have similar genotypes. Many different tests indicated the drug itself has a low response index (RI) at around .18; a low RI indicates inability of antibodies to react against DalcAA. Another immunogenicity risk assessment put DalcAA at -42.54, which is well below the average mark at 0. Essentially, all the tests say DalcAA causing nAbs was very unlikely. So then, why did these cousins react to DalcAA?

After more research, it was determined that there is a small class of people with a G128A mutation that affects less than 100 registered people in America; this means these people cannot use DalcAA. Furthermore, after several tests, ex-FDA determined that the steps CBIO took were comprehensive enough to take this drug to the next stage, Phase 2b. This Phase 2b would take into account a greater sample size to ensure the drug’s effectiveness at a greater degree. Even then, FDA and this time Europe gave DalcAA an Orphan Drug Designation (2017) for its great potential. Future tests will be done with a greater sample size where success is likely possible now that the error has been identified and fixed.

The Foot-In-The-Door Technique:

Though MarzAA and DalcAA have many promising results, Anti-C3 is another drug that is being researched and created that will hopefully be used to treat Dry Macular Degeneration (fatty deposits under the retina that cause loss of vision). Anti-C3 is a testament to the depth of CBIO’s pipeline.

FDA Process Status:

CBIO is moving quickly in its process of acquiring a FDA approval. For MarzAA, CBIO hopes to get its FDA approval by Q4 in 2019. For DalcAA, however, they are not on track for receiving FDA approval in 2019. On the other hand, the two drugs should receive approval from all major international associations of Hemophilia by Q3 of 2019, where most of these associations have already expressed approval in 2018. Thus, I feel there should be no fear of the delay in DalcAA’s FDA approval.

People:

CBIO’s executive team has leaders from different parts of the business giving the company a cross functional experience in the product development, FDA process management, corporate finance, and new product rollout.

Dr. Nassim Usman, PhD-President and CEO:

Dr. Usman has twenty-six years of experience in biotech field in the areas of hematology area working in institutions such as MIT, RPI, Sirna Therapeutics.

Dr. Howard Levy, MBBCH, PhD, MMM – Chief Medical Officer:

Dr. Levy brings eighteen years of Hematology experience to the company. His past experience in biotech and pharma leaders such as Lilly, novo nordisk, CSL, and Sangart will help in the clinicals stages of the product and while addressing FDA process.

Fletcher Payne – Chief Financial Officer

Mr. Payne brings twenty six years of field and financial experience to the company. His past experience includes companies such as Abgenix, Dynavax, Cell Genesys, and Rinat. His biotech experience and financial industry insights will help with securing the CBIO’s finances.

Mr. Andre Hetherington, SVP Technical Operations, Dr. Gant Blouse, VP Translational Research, and Jeffrey Landau, VP Business Development bring twelve to twenty years of industry experience to give the company a strong framework to execute the business.

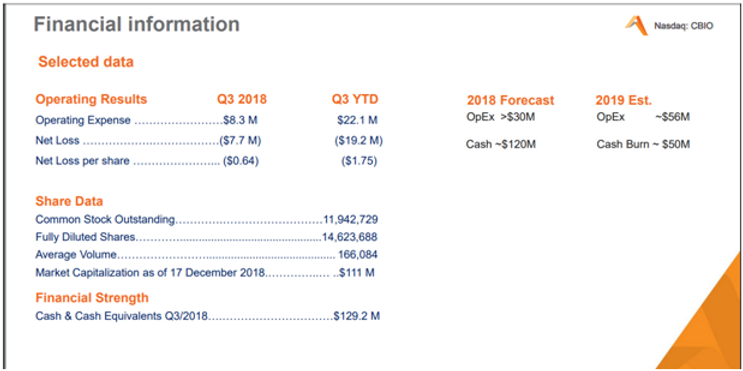

Financials:

In such a flummoxed state of financial markets, a lot of good investments are being bid lower. CBIO is not immune to the market’s shellacking. However that has created a great entry point into CBIO at the current financial levels. Although full approval for the company’s primary product, MarzAA, and the much bigger product (by market size) DalcAA are yet to get full FDA approval, the science and path towards approval from the analysis shows great promise.

Source: catalystibiosciences.com; December 17, 2018.

With product future on track, the company’s financials are not bad either. Funding of approximately $50MM to support product trials and FDA approval towards the end of the FY 2019 is secured due to the cash and cash equivalents of approximately $129MM. With a cash burn rate of $50MM per year, the company can comfortably complete the expected milestones with ease. At the end of the day, an investor into CBIO is basically getting paid to own exposure to its drug pipeline which in of itself is promising.

Institutions hold approximately 77% of shares giving the equity some strong backing from top investors such as Acuta Capital Partners LLC, Nexthera Capital LP, Blackrock Inc., Point72 Asset Management, L.P., and Renaissance Technologies, LLC. [reference: Yahoo Financials]

If the results for the Phase 2B trial turn out to be stronger than expected, a big pharma might step in to invest in the company for their 133 patents all across the globe and the future market share on the unique drug and delivery mechanism for all age groups, giving CBIO a boost in market value. The progress in trials also gives other investors an opportunity to take a stake in the company at its infancy before the end of year 2019 heading towards final FDA process.

So what does the upside look like from here? If either MarzAA or DalcAA show the potential to be a fully approved product, CBIO’s fundamental value is much higher than it is now. Orphan drug manufacturers, such as CBIO, often receive premium valuations (take Sanofi’s $11B acquisition of Bioverativ in early 2018, a 9.5x premium multiple of Bioverativ’s valuation pre acquisition). If we assume MarzAA and DalcAA each have the potential to be a $200M/year drug, a relatively modest 5x sales would support a billion dollar valuation for either assets. Risk adjusted and discounted back to present value (10 years at 10% discount rate is about a 60% discount), we have $400m in un-risk adjusted PV. This means that if CBIO can convince investors that one of their two drugs has a 25% chance of making it to market, then the market valuation should increase by $100m, or double in value.